Latest News

Paying for Vapes Using Bitcoin and Other Cryptocurrencies

Nowadays, the use of conventional cigarettes has been replaced by vaping gadgets, which are mostly used by the youth. Since some countries have embraced the new change, it is now possible for vapers to purchase whatever they need using cryptocurrencies.

So, what is so interesting about the relationship between online retailers and bitcoin? Continue reading to understand more about how you can pay for vapes using cryptocurrencies.

Benefits of Using Bitcoin and Other Cryptocurrencies

International application

The good news is ...

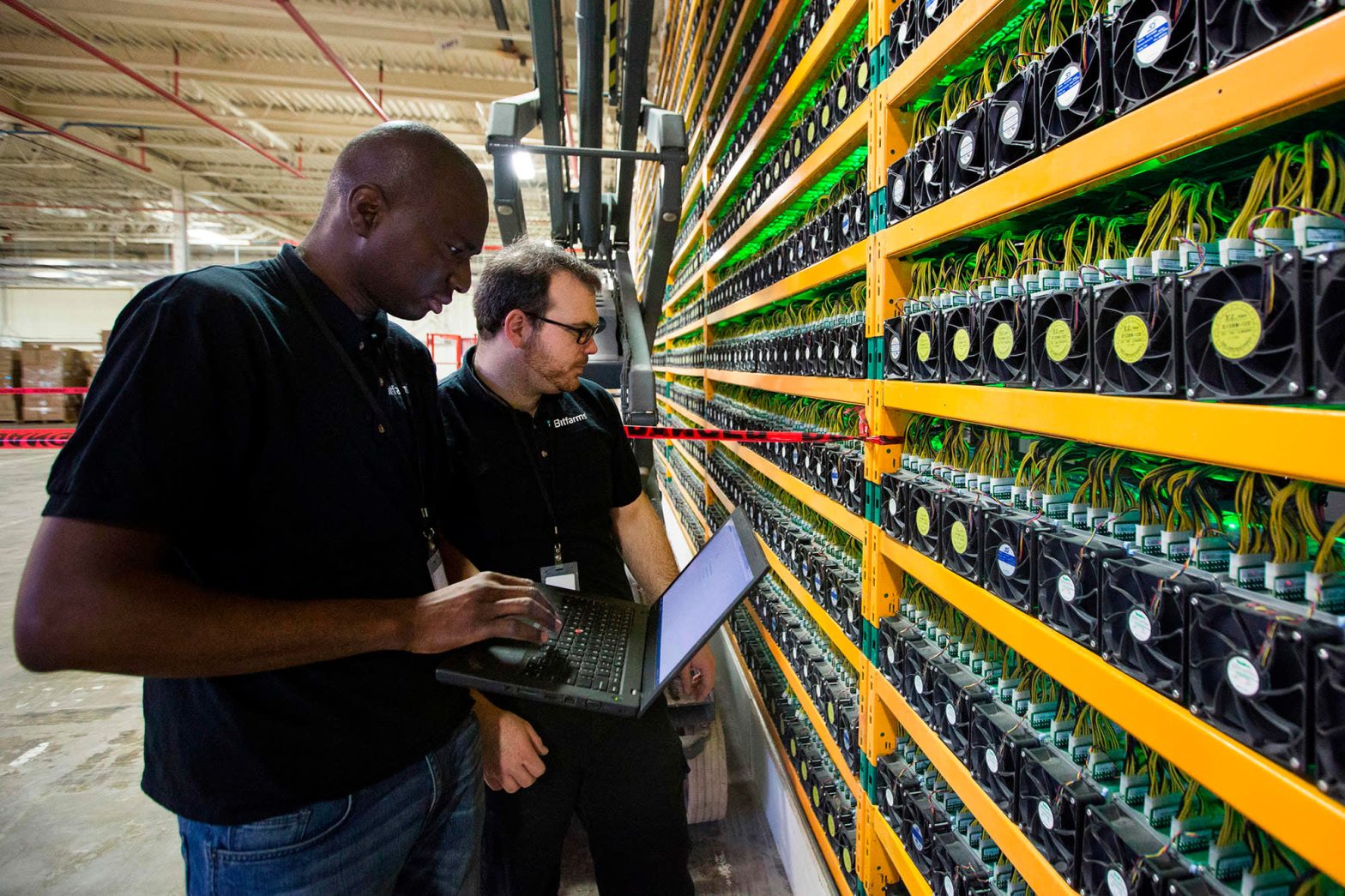

Nasdaq Cautions Crypto Mining Farm on Share Price Deficiency

Bitfarms, a Canada-based Bitcoin mining farm, faces compliance hurdles over its Nasdaq listing because of a cryptocurrency issue in progress.

On December 13, 2022, Bitfarms got a warning from Nasdaq because its share price stayed below one dollar ($1.00) for the past 30 working days. A day later, the Canadian Bitcoin mining farm announced that it has a preparatory 180-calendar-day period to reclaim Nasdaq requirements compliance.

For the compliance reclamation to proceed seamlessly, Bitfarms’ shares must close ...

Some Canadians Show Intention to Buy Cryptocurrency by 2024

In October 2022, the Ontario Securities Commission (OSC) published a report highlighting cryptocurrency adoption rates throughout Canada.

Grant Vingoe, the regulator’s chief executive, emphasized the Commission’s tech-neutral stance on cryptocurrency while mentioning that over 30 percent of Canadians plan on purchasing crypto and becoming holders soon.

On October 6, Vingoe made a keynote address in front of the Economic Club of Canada. He said that the regulatory essence of stocks and bonds is evenly ...